Commercial vehicle insurance isn't just a good idea—it's the law. These requirements are the minimum coverage levels you must carry to legally operate your business vehicles, set by federal, state, and even local authorities. Think of them less as a suggestion and more as a non-negotiable prerequisite for getting on the road.

The whole point is to make sure your business can actually cover the costs of an accident, protecting the public while also safeguarding your own financial future.

Decoding Your Insurance Blueprint

Imagine your insurance policy is the blueprint for your company's on-road safety. Just like a building can't stand without a solid foundation, your business can’t withstand the financial shock of a major accident without the right insurance. The legal requirements are the absolute ground floor of that structure, designed by lawmakers to prevent a single incident from causing catastrophic losses.

At its core, this is all about protecting the public. When a commercial vehicle crashes, the potential for serious damage and injury is incredibly high. If a business isn't properly insured, victims could be stuck with staggering medical bills and repair costs. Meanwhile, your company could be driven into bankruptcy by just one lawsuit.

The Foundation of Liability Coverage

The absolute heart of every commercial vehicle insurance policy is liability coverage. This is the concrete foundation everything else is built on, and it's legally required almost everywhere. Its job is simple: to pay for the other person's losses—their medical bills, their property damage—if your driver is at fault in an accident.

This coverage creates a crucial financial safety net, making sure there's money available to make things right for anyone who was injured or had their property destroyed. It’s what keeps commerce moving responsibly on our shared roads.

Before we dive deeper, here's a quick look at the core components that make up a compliant policy.

At a Glance: Your Core Insurance Requirements

This table breaks down the fundamental pieces of your required insurance, showing what they do and who makes the rules.

| Component | What It Protects | Who Sets the Rules |

|---|---|---|

| Bodily Injury Liability | Covers medical expenses, lost wages, and pain & suffering for people injured by your vehicle. | State governments, and for interstate commerce, the Federal Motor Carrier Safety Administration (FMCSA). |

| Property Damage Liability | Pays for repairs or replacement of another person's property (like their car, a fence, or a building) that your vehicle damages. | State governments and the FMCSA. |

| Combined Single Limit (CSL) | A single pool of money that combines both bodily injury and property damage liability into one total coverage amount. | The minimum limit is set by state and federal authorities, but you can always opt for more. |

Having a firm grasp of these basics is the first step toward building a truly protective policy for your business.

Navigating the Rules of the Road

One of the trickiest parts is that the rules change depending on where you operate. Federal, state, and sometimes even city governments have their own say, creating a complex web of regulations.

For example, a truck that crosses state lines often needs at least $750,000 in liability coverage just to satisfy federal law. But many states demand even higher limits for vehicles operating only within their borders. Staying on top of these shifting requirements is critical, and you can learn more about where the industry is headed by exploring the commercial auto insurance market outlook.

The legal mandates are not just about compliance; they are about responsible business ownership. Viewing your insurance as a critical operational asset, rather than just an expense, is the first step toward building a resilient and successful transportation enterprise.

Ultimately, meeting these legal minimums is just the starting point. From there, you can add endorsements and increase your limits to build a policy that truly protects your assets, your team, and your reputation from the countless risks out there on the road.

Understanding Your Core Coverage Mandates

Think of your commercial vehicle insurance policy as a team of specialized defenders, each with a very specific job. The law sets the minimum number of players you need on the field, but knowing what each one actually does is the key to building a truly protective strategy. It's the difference between just buying a policy and making a smart investment in your business's future.

The core of any policy is built around a few essential coverages. Each one is designed to tackle a different kind of risk, and together, they create the financial foundation that keeps you secure on the road. Let’s break down what these mandates really mean, so you know exactly what you’re paying for and why it matters so much.

Liability: The Shield for Your Business

At the absolute center of all commercial vehicle insurance requirements is liability coverage. This isn't just one thing; it's a two-part shield that protects your business from the kind of lawsuits that can be financially devastating if your driver is at fault in an accident. One bad incident could put everything you've built at risk.

This shield has two critical components:

- Bodily Injury (BI) Liability: This is what pays for injuries or, in the worst-case scenario, death that your driver causes to other people. It’s not just about medical bills—it also covers things like lost wages and the legal fees that come with a lawsuit.

- Property Damage (PD) Liability: This part pays to fix or replace someone else's property that your vehicle damages. Most of the time that means another car, but it could just as easily be a storefront, a fence, or city infrastructure.

Liability coverage is your first and most important line of defense. When an at-fault accident happens, this is the coverage that steps in to handle the other party's expenses, keeping those costs from draining your business's bank account.

This coverage is non-negotiable—it's legally required in almost every state. While the law dictates the minimum limits, smart operators, especially in the luxury transport business, carry limits far higher than the bare minimum. It’s the only way to truly protect your assets.

Protecting Your Most Valuable Assets: The Fleet

Liability coverage is all about protecting you from claims made by others. But what about protecting your own vehicles? Your fleet isn't just a collection of cars; it's one of your most valuable business assets. You need to insure your vehicles just like a contractor insures their expensive tools. That’s where physical damage coverage comes in.

This protection is also a two-part system:

- Collision Coverage: This pays to repair or replace your vehicle after a collision with another object, whether that's another vehicle or something stationary like a guardrail. Crucially, it applies no matter who was at fault.

- Comprehensive Coverage: Think of this as the "life happens" coverage. It handles damage from nearly everything else—theft, vandalism, fire, hail, or even hitting a deer.

For a business like Max's Luxury Rides Inc., where the immaculate condition of the fleet is central to the brand, physical damage coverage isn’t just an option. It's a business necessity.

Your Financial Safety Net for Unforeseen Gaps

You can have the best insurance policy in the world, but that says nothing about the other drivers on the road. What happens when you’re hit by someone with no insurance, or not enough to cover the damage they caused? It’s a more common scenario than you might think, and without the right protection, you're the one left holding the bills.

This is exactly why Uninsured/Underinsured Motorist (UM/UIM) coverage is so vital. It’s your financial safety net, stepping in to pay for your expenses when the at-fault driver's insurance is either missing or maxed out. Depending on your state, it can cover medical bills for you and your passengers and even repairs to your vehicle.

Finally, there’s one more layer of immediate protection. Medical Payments (MedPay) or Personal Injury Protection (PIP), depending on where you operate, covers medical bills for you and your passengers right after an accident, regardless of who is at fault. This ensures everyone can get the care they need immediately, without having to wait for a lengthy and often stressful fault determination process.

Navigating Federal, State, and Local Liability Limits

Think of your commercial insurance requirements like a set of nesting dolls. The outermost doll is federal law, but once you open it, you find state regulations inside. Open that one, and you might find even more specific city ordinances. To be fully compliant, your coverage has to satisfy the rules of every single layer.

This tiered system exists for good reason—ensuring public safety and financial responsibility. But it definitely puts the pressure on business owners to know the exact rules for every single place they operate. A policy that's perfectly fine in one county could leave you dangerously exposed just a few miles down the road.

The Federal Baseline for Interstate Commerce

If your vehicles cross state lines, your starting point is always the Federal Motor Carrier Safety Administration (FMCSA). The FMCSA sets the absolute floor for liability coverage for anyone engaged in interstate commerce. This creates a national minimum, a basic level of protection that applies everywhere in the U.S.

For most businesses, the key number to know involves general freight.

- For non-hazardous freight in vehicles over 10,001 lbs: The minimum required liability coverage is $750,000.

- For hazardous materials: The limits shoot up dramatically, often to $1,000,000 or even $5,000,000, depending on what you’re hauling.

That $750,000 isn't just a random number; it reflects the catastrophic damage a large truck can cause in a major accident. But here’s the most important takeaway: treat that number as the starting line, not the finish line.

How States and Cities Add Their Own Rules

While federal rules cover the highways between states, each state gets to write its own rulebook for businesses that operate solely within its borders (intrastate commerce). A state might decide the federal minimum isn't enough and demand higher liability limits or specific extra coverages.

And it can get even more granular. Large cities often pile on another layer of regulations. For a Chicago-based limousine company like Max's Luxury Rides Inc., the city’s rules are just as critical as any state or federal mandate.

Local regulations are often the most demanding because they’re designed for the unique risks of a crowded, fast-paced urban environment. Get them wrong, and you’re looking at hefty fines, a suspended operating permit, or total financial ruin after an accident.

This is precisely why a generic, one-size-fits-all insurance policy is such a liability. Your coverage has to be built to meet the highest standard required anywhere you do business, from a federal interstate to a downtown side street.

A Real-World Example: Chicago's Livery Laws

Let's see how these layers stack up in the real world by looking at the rules for livery vehicles in Chicago. The city has its own specific insurance minimums that are completely separate from Illinois state law and federal regulations.

The table below gives you a clear snapshot of how these requirements can differ.

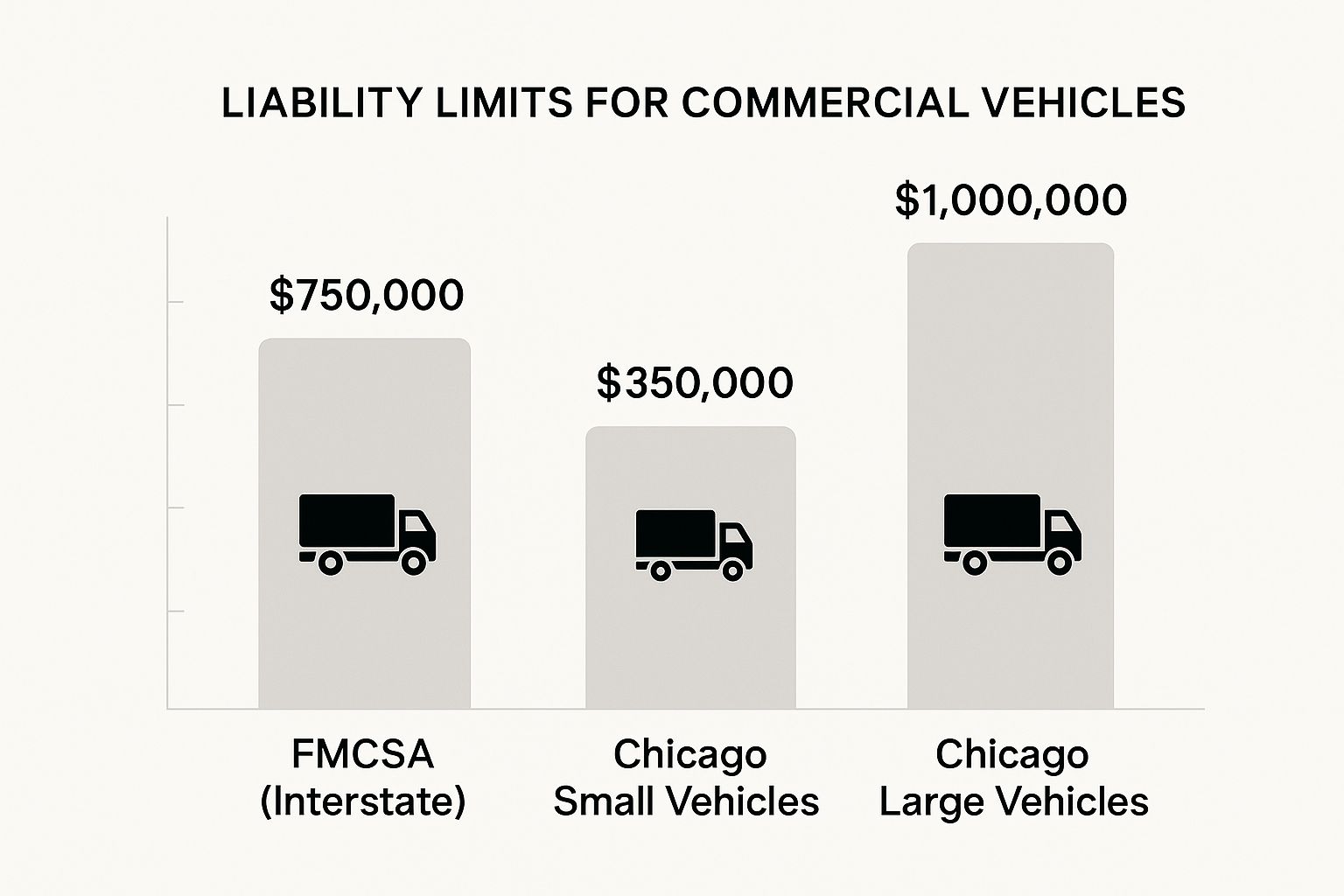

Liability Limits Compared: Federal vs. State vs. City

This table illustrates how insurance requirements for the same type of vehicle can vary dramatically across different jurisdictions.

| Jurisdiction | Example Liability Requirement | Applies To |

|---|---|---|

| Federal (FMCSA) | $750,000 | Non-hazardous freight vehicles over 10,001 lbs operating across state lines. |

| City of Chicago | $350,000 | Small livery vehicles (1-8 passengers) operating within city limits. |

| City of Chicago | $1,000,000 | Large livery vehicles (9-15 passengers) operating within city limits. |

As you can see, simply meeting the federal minimum wouldn’t be nearly enough for a large limousine operating in Chicago.

The infographic below visualizes this difference perfectly.

This chart makes it crystal clear: a Chicago limousine operator has a completely different set of rules to follow than an interstate trucker just passing through.

For livery services in Chicago, the rules are broken down by passenger capacity:

- Small Livery Vehicles (seating 1-8 passengers): A minimum of $350,000 per-occurrence liability coverage is mandatory.

- Large Livery Vehicles (seating 9-15 passengers): The requirement skyrockets to a $1,000,000 combined single limit.

This complexity is a major driver behind the growth of the commercial auto insurance market. Valued at roughly USD 151.98 billion in 2025, it’s expected to hit USD 199.46 billion by 2029, a trend fueled by the need for expert guidance and specialized coverage. You can read more about the growth of the commercial vehicle insurance market to see where the industry is headed.

Staying on top of your commercial vehicle insurance requirements isn’t a one-time task; it's an ongoing job. The smartest move any operator can make is to work with an insurance pro who lives and breathes this stuff—someone who knows your industry and your city inside and out. That's how you build a policy that truly protects your business.

Don't Forget to Add Essential Policy Endorsements

A standard commercial auto policy is a great starting point, but it's rarely enough to fully protect your business. Think of it like a new truck straight off the factory line; it's got the engine and wheels, but it’s missing the custom tool racks, liftgates, and other gear you need to actually do your job.

Policy endorsements (sometimes called riders) are those custom upgrades. They’re not just fancy add-ons; they’re often critical for plugging the specific gaps in a standard policy. Without the right ones, you could be driving around with some serious—and very expensive—blind spots in your coverage.

Covering Vehicles You Don't Actually Own

One of the riskiest assumptions any business owner can make is thinking their policy covers any and every vehicle used for work. What happens when you have to rent an extra limo for a big wedding party? Or an employee uses their personal car to run a quick company errand?

If you don't have the right endorsement, your standard policy won't cover you in those situations. Not one bit. That’s why Hired and Non-Owned Auto (HNOA) insurance is so crucial.

- Hired Auto provides liability coverage for vehicles your business rents, leases, or borrows.

- Non-Owned Auto protects your company from liability when an employee gets into an accident while using their own car for work.

Without HNOA coverage, a wreck in a rented vehicle or an employee’s sedan could lead to a lawsuit that comes directly after your business assets. It’s a non-negotiable endorsement for any operation where you might use vehicles beyond your official fleet.

Protecting What's Inside Your Vehicle

For many businesses, the cargo is just as valuable as the truck carrying it. A basic auto policy covers damage to the vehicle, but it does absolutely nothing for the property you're transporting. This is where cargo insurance comes in.

This endorsement protects the freight you're hauling from theft, damage, or total loss. If you’re a caterer, a courier, or anyone moving valuable client goods, this coverage is essential to meeting your commercial vehicle insurance requirements and protecting your reputation.

A policy without cargo coverage is like a bank vault with no money inside. It protects the container but ignores the valuable contents that are the entire reason for the journey.

For truckers, there's another key endorsement in this category: Trailer Interchange Insurance. This covers physical damage to trailers you're pulling but don't own—a day-to-day reality in the logistics world. It ensures you're covered if a non-owned trailer gets damaged while under your care.

Insuring Your Specialized and Attached Equipment

Your commercial vehicles are often mobile workshops packed with expensive, specialized equipment. A standard policy won’t cover the custom gear you’ve bolted onto or installed in your truck or van.

An endorsement for permanently attached equipment solves this. It extends your coverage to all the valuable assets that make your vehicle a workstation, including:

- Custom toolboxes or storage systems

- Ladder racks

- Refrigeration units

- Hydraulic lifts

Insuring this equipment properly means that one bad accident doesn't just put a vehicle out of commission—it also doesn't wipe out the essential tools you depend on to run your business. Taking the time to review your operations and add the right endorsements is what turns a basic policy into a bulletproof safety net.

How Market Risks Influence Your Insurance Premiums

If you've seen your commercial insurance premiums climb even with a perfect driving record, you're not alone. It's frustrating, but it's important to know that these increases often have less to do with your company and more to do with powerful forces shaking up the entire insurance market. Understanding these external risks gives you the bigger picture and shows why a rock-solid internal safety culture is your best line of defense.

Right now, the industry is in what’s called a hard market. Think of it like a seller's market in real estate—when demand outstrips supply, prices shoot up and sellers can afford to be picky. In a hard insurance market, insurers have been hit with massive, industry-wide losses. They’ve paid out far more in claims than they’ve collected in premiums, forcing them to get much tougher on who they’ll cover and to charge a lot more for it.

The Challenge of Soaring Claims and Repair Costs

Two major trends are fueling this hard market and hitting your bottom line. The first is the staggering rise in claim costs, often driven by what the industry calls "nuclear verdicts." These aren’t your typical accident settlements; we’re talking about jury awards in lawsuits that soar into the tens of millions of dollars.

A single verdict of that size sends a shockwave through the insurance world. It forces every provider to reassess their own risk and hike rates across the board to build up cash reserves for the next potential massive payout. The unfortunate result is that even the safest operators end up paying more to cover the risk created by these rare, but catastrophic, events.

The second factor is the skyrocketing cost of vehicle repairs. The sophisticated luxury vehicles operated by companies like Max's Luxury Rides Inc. are technological marvels. A simple fender bender isn't so simple anymore. It now means replacing or recalibrating a whole suite of complex systems:

- Advanced Driver-Assistance Systems (ADAS)

- Networks of cameras and proximity sensors

- Intricate infotainment and electronic controls

These high-tech repairs cost a fortune compared to older models, pushing the cost of physical damage claims through the roof and taking your premiums right along with them.

A Decade of Industry-Wide Financial Pressure

This isn't a new problem. It’s a storm that’s been brewing for years. The commercial auto insurance sector has endured 13 consecutive years of underwriting losses. For 12 of those 13 years, their combined loss ratios have been over 100%. In plain English, that means for over a decade, insurers have been paying out more in claims and expenses than they’ve collected in premiums.

This long-term financial bleed is a core reason premiums keep climbing. Insurers are desperately trying to get back into the black after a disastrous decade, leading to rate increases between 9% and 9.8% in the first half of 2024 alone.

In this kind of unforgiving market, you can't afford to be seen as just another number. You have to stand out as an excellent, low-risk client. To dig deeper into these trends, you can discover more insights about the state of commercial auto insurance from Conning's recent analysis.

Once you see these external pressures for what they are, the value of proactive risk management becomes crystal clear. An impeccable safety record, rigorous driver training, and meticulous vehicle maintenance aren't just good habits anymore—they are the most powerful tools you have to control your costs in an incredibly challenging insurance landscape.

Your Top Commercial Insurance Questions, Answered

Let's be honest—navigating the world of commercial vehicle insurance can feel like trying to read a map in the dark. The rules seem to change depending on your vehicle, your state, and even the type of cargo you're carrying. To cut through the confusion, we've tackled some of the most common questions we hear from business owners.

Think of this as your practical guide to making smart, confident decisions that protect your business and keep you on the right side of the law.

I Use My Personal Car for Work. Do I Really Need a Commercial Policy?

This is one of the most critical questions, and the answer is almost always a resounding yes. It’s a common—and frankly, dangerous—misconception that your personal auto policy has you covered for business use. It doesn’t. In fact, most personal policies have a "commercial use exclusion" written right into the fine print.

That means if you're doing any of the following, your personal insurance won't cover an accident:

- Transporting clients or paying passengers.

- Making deliveries or driving to sales appointments.

- Hauling tools or equipment to a job site.

If you get into a wreck while on the clock, your insurer can legally deny your claim, leaving you personally on the hook for every penny of the damages. It's a gamble no business can afford to take.

What Exactly Is a Combined Single Limit (CSL)?

A Combined Single Limit, or CSL, is the modern standard for commercial auto liability. The easiest way to think of it is as one big, flexible pot of money that can be used to cover all the damages in an accident you cause. It bundles together coverage for both bodily injury and property damage into a single, total amount.

For example, a $1 million CSL policy gives you up to $1 million to pay for any combination of costs. If a crash leads to $800,000 in medical bills for others and $200,000 in property damage, the CSL policy covers it all. This is a huge advantage over older "split limit" policies, which put separate, rigid caps on different types of damage. CSL provides far more robust protection, which is why it's the go-to for serious commercial operations.

How Can We Actually Lower Our Insurance Premiums?

While insurance rates can feel like they're completely out of your hands, you have more control than you think. The secret isn't about finding loopholes or cutting coverage—it's about proving to insurers that you are a safe, professional, and low-risk operation. A genuine commitment to safety is your single most powerful tool for managing costs.

Here are the strategies that make a real difference:

- Build a Real Driver Safety Program: Don't just check a box. Invest in ongoing training that covers defensive driving, spotting hazards, and reinforcing your company’s safety rules.

- Embrace Telematics: Install devices that track driving habits like hard braking, speeding, and sharp turns. Use that data to coach drivers who need a little help and reward the ones who set a great example.

- Get Serious About Fleet Maintenance: A well-maintained vehicle is a safe vehicle. Keep meticulous service logs to show underwriters you're proactive about preventing mechanical failures.

- Hire the Right People: Your drivers are your biggest risk. A thorough screening process that looks for clean driving records isn't just a good idea; it's essential.

Beyond that, have an open conversation with your insurance agent. Reviewing your deductible or making sure your vehicles are classified correctly can also lead to savings. A specialist agent who knows your industry can shop your policy to find the best rates from carriers that understand and value your business.

What Information Do I Need to Get an Accurate Quote?

The quality of your insurance quote is directly tied to the quality of the information you provide. The more organized and detailed you are, the more accurately an underwriter can price your risk. When you're prepared, the entire process moves faster and you end up with a much better result.

Think of the quoting process like you're pitching an investor. Your goal is to present a clear, compelling story of a well-managed, safety-first business that any insurer would want as a partner.

Before you even start the conversation, get these key items together:

- Business Identifiers: Your DOT and MC numbers, if your operation requires them.

- Vehicle Schedule: A full list of every vehicle you need to insure, including the year, make, model, and VIN for each one.

- Driver Roster: A list of every single driver, including their full legal name, date of birth, and driver's license number.

- Operational Details: A straightforward description of your business. Be specific—do you do airport transfers? Corporate events? What is your typical radius of operation?

- Claims History: This is a big one. You'll need your "loss run" reports for the last three to five years. This is the official record of any claims your business has filed, and it's one of the most important documents in underwriting.

Having this information ready to go shows you're a professional and helps your agent fight for the best possible terms on your behalf.

At Max's Luxury Rides Inc., we know that safety and compliance are the bedrock of outstanding service. For reliable, professional, and fully-insured luxury transportation in Chicago, book your next ride with us. Learn more and reserve your vehicle today.